Meet the accidental venture capitalist fuelling India's D2C boom

Kanwaljit Singh has been relentlessly stoking the direct-to-consumer fire in India. Can his Fireside Ventures stay fired up?

By Rajiv Singh

Last Updated: Apr 11, 2022, 14:43 IST12 min

Bengaluru, October, 2014.

There were quite a few suitors aggressively wooing PC Musthafa. And why not? Nine years after turning entrepreneur in 2005—when he co-founded iD Fresh Food with his cousins Shamsudeen TK, Abdul Nazer, Jafar TK and Noushad TA—Musthafa had finally relented to ‘marry’. In 2014, the ready-to-cook fresh food brand, more known for idly and dosa batter, had reached a decent scale of operations and was reportedly clocking Rs7 crore monthly sales across eight cities. For Musthafa, it was the right time to start a new innings.

There was a problem, though. The ‘bride-to-be’ was much older than Mustafa. But the age did not matter to him. “I was ‘marrying’ one of the best marketing minds in the world," recalls the IIM Bangalore alum. There was another small problem. “The ‘bride’ had a beard", laughs Musthafa. He soon got to know of a third problem: The ‘bride’ was planning to call it quits.

The news was broken by Kanwaljit Singh, co-founder and senior managing director of Helion Venture Partners. Just a few hours ahead of signing the term sheet for iD’s maiden institutional funding by Helion, Singh took Musthafa out for lunch. “I am leaving Helion," he said. Musthafa was shocked. “You can’t do this," he gasped, still reeling under the shock. Among all the investment proposals, Helion’s offer was at the bottom of the heap. “It was the least valued offer," he recalls. The only reason Musthafa went ahead with the ‘marriage’ was Singh, who was now quitting.

An agitated Musthafa was in no mood to sign the term sheet. In order to avert an impending embarrassment for Helion and Singh, Musthafa bargained for his pound of flesh. “I will sign the term sheet but you have to be on my board as an independent director," he said. “And you have to be there as long as I want," he stressed. Singh agreed. Helion pumped in Rs35 crore in October 2014.

*****

Four years back in 2010, Neeraj Kakkar had landed in Bengaluru. The MBA grad from the Wharton School in the US had close to seven years of work experience with Coca-Cola India, and now had Singh as his boss during his summer internship at Helion. “He was inspirational," recalls Kakkar, who worked on a couple of consumer brand projects with Singh. A few months later, he got a job with McKinsey in the US, but Singh encouraged him to start his own venture. The disciple did not know what the guru had spotted in him, but he obliged. Naturally, Helion was the first port of call to raise money for the yet-to-be born venture. “Would Helion invest," asked Kakkar, who decided to start a protein drinks’ business with his friend Suhas Misra.

Singh was excited to back the nebulous idea. But Helion, as a fund, declined. The reason was simple. For Helion, which was known more to fund tech ventures, getting into consumer business would have pushed it away from its core. Second, back in 2010, startup ecosystem in India was still in the kindergarten days. And not many were willing to punt on ideas that were either non-existent or sounded outrageous to begin with.

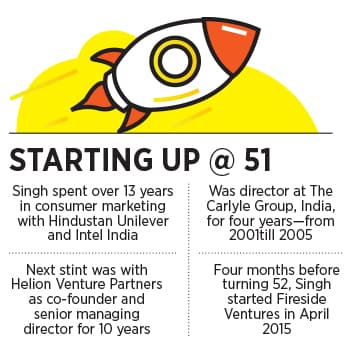

Singh was miffed. “If Helion is not funding," he declared, “I will put in my money." The venture capitalist, who spent over 13 years in consumer marketing with Hindustan Unilever and Intel, and another four years as a funder with Carlyle Group before joining Helion in 2005, wrote Kakkar cheque of Rs25 lakh. This was his first individual investment.

How do you explain backing a non-existent business, or spotting railway tracks when there were no railways? In fact, what Kakkar had, he confesses, was just a figment of protein drinks in his head. Singh, though, was thinking from his heart. “He was passionate. I knew he would figure it out," he reasoned, explaining what made him back his instinct. The most important thing for him, Singh underlines, is the excitement in the eyes of the founders when they talk of the ideas. “This might sound silly but I am a very instinctive VC," he says.

Six years later, in August 2016, Singh’s instincts made his heart pound again with hyper excitement. By now, the veteran VC had quit Helion and registered Fireside Ventures’ Trust as his personal family office entity through which he was scouting for raw diamonds.

Working out of coffee shops—staff at The Leela in Bengaluru still recognise the turbaned man—Singh was living his dream by backing the dream of young founders. Two such day-dreamers were Varun and Ghazal Alagh. The husband-wife duo wanted to make toxin-free baby care products, and take them directly to consumers. The idea sounded amusing. Reason: Not many cared about toxin-free products, which means the market for such offerings could be niche. Varun, who had worked at Unilever, Coca-Cola and Diageo, managed to use his Unilever connect to reach out to Singh.

The meeting started at The Oberoi in Gurugram. While Varun did his best to hide his nerves, Ghazal, who had earlier founded Dietexpert, a startup customising diet plans, talked passionately about the products that the yet-to-be-born venture would make. After 30 minutes came a two-word reply. “Theek hai (okay)," said Singh. “I am in."

The meeting started at The Oberoi in Gurugram. While Varun did his best to hide his nerves, Ghazal, who had earlier founded Dietexpert, a startup customising diet plans, talked passionately about the products that the yet-to-be-born venture would make. After 30 minutes came a two-word reply. “Theek hai (okay)," said Singh. “I am in."

Varun was excited, and tried to offer more meat. “Would you like to have a look at excel sheet and business plans," he asked. Singh smiled. “I do not need it." He then shared his feedback. First came the shocking disclaimer. “I don’t know if you guys would end up doing what you plan to do," he said with a poker face. Then came the assurance. “But what I know is that you guys are nice and am sure you will do something good," Singh underlined.

For the venture capitalist, the golden rule of investment has been to bet on jockeys, not the horses. “Do we have 10 Mamaearths or Paperboats [co-founded by Kakkar]," he asks. According to Singh, the answer is in the quality of the founders and the founding team. “It is always jockeys who change the game," he says, adding that the only thing he hunts for in founders is passion. “One has to be insanely obsessed with the idea."

His sole question for aspiring founders is: Are you doing it just because you want to give it a shot, or are you all in? “It has to be a life-and-death situation. The rest can be taken care of," says Singh, who is an accidental VC. His colleague at Intel had quit and joined Carlyle Asia as a venture partner. He reached out to Singh and roped him in. “That’s how my VC journey started."

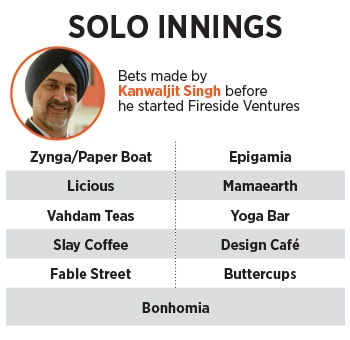

Though Singh stayed at Carlyle for four years, his tryst with personal investing happened once he joined Helion. During his decade-long stint till 2015, he backed over a dozen consumer brands such as Paperboat, Epigamia, Licious, Mamaearth, Vahdam Teas and Yoga Bar. As the investment was from personal money, the ticket size was small—between Rs25 lakh and Rs50 lakh.

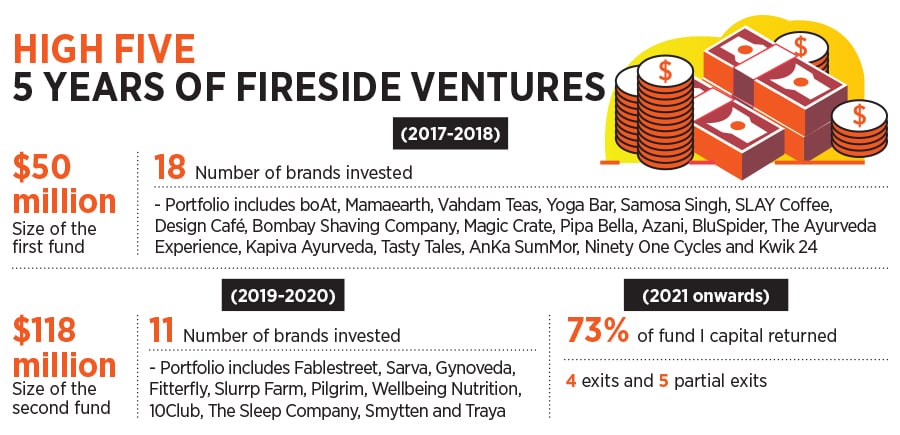

The stake picked up was also, therefore, tiny—from one percent to three percent. With the rollout of an institutional fund from 2017 onward—Fireside Ventures closed the first fund at $50 million—Singh stopped personal investments and embarked on a journey of marrying his passion with the obsession of founders to stoke the fire of direct to consumer (D2C) brands in India.

The new journey for Singh’s early-stage consumer-focused fund began on a fresh investment note. Cheque size got beefed up and now ranged between Rs3.5 crore and Rs7 crore, and Fireside picked up a minimum stake of 10 percent.

While a bunch of startups such as Mamaearth, Vahdam Teas and Yoga Bar, in which Singh has invested in personal capacity, found backing from the fund, Fireside started to make distinctive and bold bets in the consumer space with boAt, Ninety One Cycles, Bombay Shaving Company and Samosa Singh.

What also changed was the way Singh moulded Fireside. Though instinctive bets still formed the core, investments got more structured and methodical. The founders now pitching to an institutional investor like Fireside, explains Singh, need to play in a large market that can be disrupted.

What also changed was the way Singh moulded Fireside. Though instinctive bets still formed the core, investments got more structured and methodical. The founders now pitching to an institutional investor like Fireside, explains Singh, need to play in a large market that can be disrupted.

‘Can you build a disruptive business which can scale and sustain that disruption over time’ is what Singh and his team started asking the aspirants. Second crucial element, he lets on, is having a differentiated product. “Do you have enough fuel to keep the innovation engine on fire" is the next question for the entrepreneurs. Though the second fund of Fireside doubled its corpus size—$118 million—it only invested in 11 startups as against 18 backed by the first fund.

Singh explains why the numbers dipped, and what has changed. The most interesting shift has been in terms of the ticket size of investment. Fireside now picks up at least 20 percent stake, and the cheque size ranges from Rs7 crore to Rs14 crore, and the fund invests in startups that are clocking a revenue of around Rs50-60 lakh per month.

In terms of valuations, these businesses would be typically valued around Rs30-40 crore. “Now this is our sweet spot," says Singh, who is quick to paint a realistic picture of the returns expected. After all, a fund needs to make money. “We might not get a 50x or 100x every time," he says, adding that the idea is to get 5x or 10x in 50-70 percent of the cases. “It then becomes a very powerful story," he says. The fund, he underlines, does seven-eight deals every year, and stays away from over-speeding.

A sedate pace of investment also made Fireside more structured. “My best deals," says Singh, referring to his personal investment days, “were not been based on some fancy thesis. I am being honest".

Now with Fireside morphing into an institutional fund, the team expanded and roles evolved. Though Singh might be still calling the shots, the fund is not a one-man show. “I cannot be the guy who will be there 20 years later," he says, explaining the move to rope in Vinay Singh, VS Kannan Sitaram and Dipanjan Basu.

In fact, while adding more members to his team, he explained how he was planning for devolution of power. “Today, I am driving the car and you guys are in the backseat," he told his team. A fund or two later, all would be co-drivers. “And then at some point, you start driving and I will take the backseat."

Though the seasoned driver has had a smooth ride so far, Singh too has had his lapses. “At times, my biases might have become a constraint," confesses Singh.

Atomberg, for instance, is one such case. Singh had the consumer appliance startup on his radar for a while, and the Fireside team too found the venture promising.

“They were the classic case of engineers using great technology and building great products," he says. But Fireside did not invest. Reason: Singh had his biases around the startup’s ability to build a distribution system and network. “Unko business aata hai, lekin kya distribution bhi aata hai? (They know business but do they also know distribution?) was the question for which Singh could not find a convincing answer. The result was a miss.

The other notable miss was Licious. “It was my judgement call," rues Singh, explaining the backstory. During the early days of Fireside as a fund, there was an opportunity to make an investment. Though the meat startup had multiple term sheets, the co-founders were keen to make space for Fireside as Singh had invested in the company in a personal capacity. There was only one small problem. The startup then had Rs200-crore valuation, and Fireside would have ended up getting a low single-digit stake. “It was a new fund, and steep valuation was the only irritant," he says.

Then there were misses when an investment did not do well. Take, for instance, Pipa Bella. The online jewellery brand was started by Suchi Pandya in 2013. “The company was doing well, ramping well, and then Covid happened," says Singh, adding that the venture was hit on two fronts. First, the demand evaporated as work-from-home almost killed the need to buy fashion jewellery. Second, the production ecosystem—around Mumbai—shut down. “The business just collapsed," he says, adding that he was quite close to the brand and the founder happened to be one of the best brains he has worked with. Last April, Pipa Bella was bought by Nykaa.

Another miss was when one of the ventures got badly hit due to co-founders’ conflict. “It was an innovative business but the feud did the damage," says Singh, declining to disclose the name of the company. Founder conflict, he underlines, has been one of the biggest challenges that Singh has faced over the last two decades.

What about the potential challenges? Does Singh see exaggerated valuations and funding spree as strong headwinds that might damage the consumer brands story in India? “Both are disturbing trends," he says, explaining how cracks can change into serious ruptures for the startup ecosystem.

During the initial days of Fireside, a bunch of tech VCs would keep asking Singh about the growth of the consumer brands in his portfolio. “30 percent month-on-month growth hota hai ki nahi (do they grow 30 percent m-o-m)," was the question. Singh knew it was a warning bell. “30 percent month-on-month growth is the biggest death knell for the industry," he says.

Valuation and performance end up becoming a vicious circle. If you are getting money which, let’s say, values company two years ahead of the curve, then the pressure to justify the numbers would be huge. The business model of Fireside, Singh explains, is predicated on two things.

“First is that we will not over-capitalise you," he says, adding that he can write three different cheques at three different times and will keep writing bigger cheques. “But I will never have that ability to write a first cheque so large that I start encouraging this kind of behaviour," he says. Second is sharp focus on unit economics. “We want to see high gross margin businesses," he says. The bad behaviour of over-capitalising and higher valuation, he lets on, is unfortunate.

Let’s take the example of beauty and personal care segment. Due to the success of Mamaearth, Nykaa and others, a bunch of me-too brands have exploded. “People have now started writing crazy cheques and at crazy valuations. You cannot build a business like as a house of cards," he says. Building good business, he underlines, takes time.

Singh, meanwhile, talks about his time in a different context. “I have been on the board of iD as an independent director for long," he smiles. “I think now it is time over for me to exit." Mustafa, for his part, cannot think of ending the ‘marriage’, as it has worked well. “I am in no mood to divorce," he smiles.

First Published: Apr 11, 2022, 14:43

Subscribe Now