“The greatest risk in the near term is the potential for policy error," says Steve Cochrane, chief economist, APAC, Moody’s Analytics.

![]()

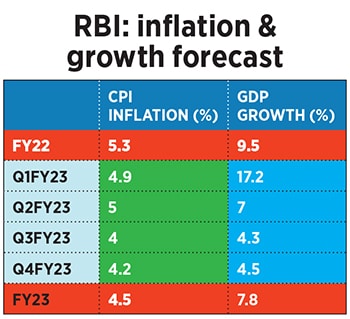

The Reserve Bank of India (RBI) had estimated inflation to peak at 5.7 percent in the fourth quarter of the current fiscal year. It may need to revisit its inflation and growth forecasts in light of the recent geopolitical developments (see chart).

Aditi Nayar, chief economist, ICRA, believes that inflation is moving north mainly due to the surge in international commodity prices, and supply side factors, pushing up input costs, rather than robust domestic demand.

“The RBI MPC can go ahead and tighten rates sharply, but will that fundamentally change global crude oil prices?" Nayar asks rhetorically. Domestic monetary policy response will not change what is happening in the global commodity market, she reasons.

![]()

In a bid to tackle high inflation, the US Federal Reserve hiked interest rate by 25 basis points in March, and has signalled a series of rate hikes in the coming quarters. The Reserve Bank of India isn’t humming a hawkish tune yet, but is widely expected to signal a shift towards policy normalisation.

Saugata Bhattacharya, chief economist, Axis Bank, says the monetary policy response will depend on the space available to fiscal policy to absorb some of the price and income impact. “We believe that this is not the time to start normalisation, given the pervasive uncertainty on almost every aspect of the economy," he adds.

Varma is of the view that the RBI must act upon inflation sooner rather than later, in order to not end up hurting medium-term growth prospects, or playing catch-up on rate hikes later, as it is unlikely that inflation will cool down to a 4-5 percent level in the next six to nine months.

![]() “Ultimately monetary policy has to do a cost benefit analysis how much are we incrementally supporting growth through our policies versus how much are we risking future growth because of accommodating a higher inflation for so long. It is better to move early than having to do a larger pivot down the line," explains Varma.

“Ultimately monetary policy has to do a cost benefit analysis how much are we incrementally supporting growth through our policies versus how much are we risking future growth because of accommodating a higher inflation for so long. It is better to move early than having to do a larger pivot down the line," explains Varma.

Clamp down on inflation

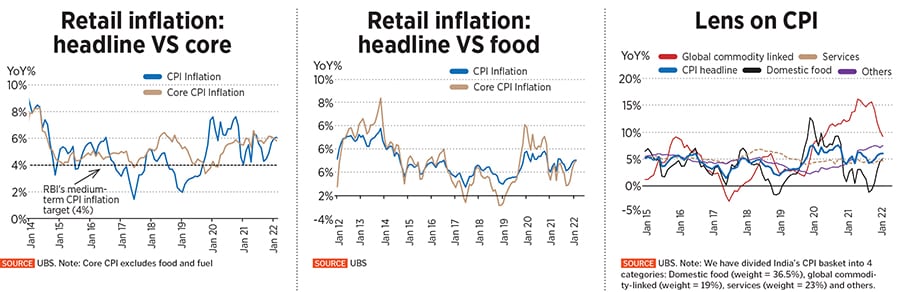

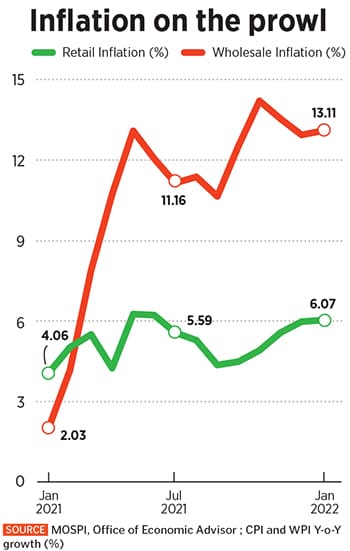

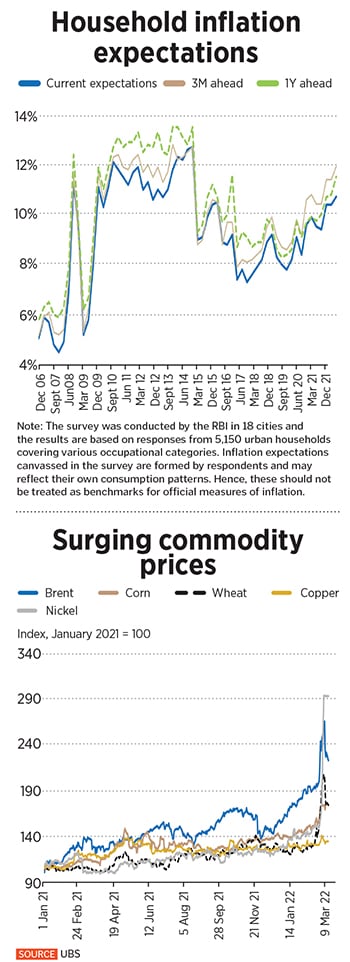

Spiralling inflation has been a major concern for many months (see chart). However, in the past two months it has breached 6 percent with no signs of cooling off in a hurry. While the wholesale price index (WPI) has been on a tear for over one year, over 60 percent of consumer price index (CPI) core constituents inched up to around 6 percent in February.

“Inflation is a rising risk in India. The country has the highest inflation rate among large Asia-Pacific economies. It also appears to be broad-based and in particular embedded in food prices. Further, given the rise in global energy prices since the Russia-Ukraine military conflict, inflation might climb up further in the months to come," says Cochrane.

Given the rise in global oil and commodity prices (see chart), it is not clear yet that inflation has peaked, but, if the RBI feels compelled to raise interest rates, it would weigh on the economy, he adds.

The jump in input costs has translated into higher production costs which has been partly passed on to consumers leading to higher price levels across most categories of goods and services.

“Persisting high levels of headline and core inflation have indeed emerged as a concern, especially after the shocks to energy, metals, food and other commodities prices," agrees Bhattacharya.

![]() Economists have revised their inflation target upwards in light of the volatility in the commodity price cycle in the backdrop of high uncertainty.

Economists have revised their inflation target upwards in light of the volatility in the commodity price cycle in the backdrop of high uncertainty.

“Our FY23 average inflation forecast is 5.8 percent, with some upside risks, but the trajectory is likely to be falling over FY23, largely due to the base effects of high inflation in FY22. However, Q1 FY23 inflation is likely to remain at or above 6 percent," says Bhattacharya.

Varma pegs inflation at around 6.2 percent in the current calendar year. She explains, with underlying inflation hovering at around 5.5 percent, the various supply side shocks and adjustments in fuel prices will drive up global food prices, and have a spill-over effect on domestic prices.

The increase in the landed price of imports is expected to get rapidly transmitted into wholesale inflation. As for retail inflation, fuel prices, gold prices and edible oil prices will weigh on the consumer price index.

The lack of clarity on how long the war in Ukraine will continue, and how the sanctions on Russia play out, has meant there is no clear-cut inflation trajectory for guidance.

“If the Russia-Ukraine conflict can reach some resolution by mid-year, then the risk premia now embedded in many commodities will narrow, commodity prices will return closer to their pre-conflict levels, risks of supply-chain constraints will ease, and economic growth could accelerate once again in the second half of this year," says Cochrane.

![]()

Give growth a chance

India is a net commodity importer, and the current headwind of high commodity prices poses adverse risks for the domestic economy’s fiscal health. These factors stand to potentially nip the green shoots of economic recovery as consumption spending and private investments take a hit.

“As long as the rise in commodity prices is not a long-term trend, consumer spending and investment should improve with the global economy," says Cochrane. “A turnaround in manufacturing and services would suggest that a release of pent-up demand could power the economic recovery. But the risk is that fears of inflation, or of another Covid wave could limit spending and the re-entry of labour into the workforce," he adds.

![]() Importantly, the investment cycle needs to kick-start to spur durable recovery. Most manufacturing hubs are not operating at full capacity utilisation levels, thereby pent-up demand may not be sufficient to incentivise fresh investments for expansion.

Importantly, the investment cycle needs to kick-start to spur durable recovery. Most manufacturing hubs are not operating at full capacity utilisation levels, thereby pent-up demand may not be sufficient to incentivise fresh investments for expansion.

“Durable recovery is a challenge. There are policy trade-offs here, so the (geopolitical) shock is going to mean higher inflation and lower growth," says Varma. “It is not a stagflation (scenario), but it is a stagflation type effect of the current global macro backdrop and it does mean lower growth and higher inflation," Varma adds.

However, as the economy limps back to normalcy after the third wave of coronavirus infections, the re-opening of travel, tourism, and hospitality sectors can serve as a catalyst to growth. Nomura’s Varma expects GDP growth of 7.5 percent in FY23 and around 5.5 percent in FY24.

![]() Bhattacharya says there are anecdotal indications of capex plans among MSMEs. He points to strong exports, ancillary signals like bank credit and e-way bills to suggest an uptick in economic activity. “We forecast India’s FY23 GDP growth at 7.8 percent, but there is a strong downside risk to this, which is difficult to quantify given the extreme uncertainty at present," he adds.

Bhattacharya says there are anecdotal indications of capex plans among MSMEs. He points to strong exports, ancillary signals like bank credit and e-way bills to suggest an uptick in economic activity. “We forecast India’s FY23 GDP growth at 7.8 percent, but there is a strong downside risk to this, which is difficult to quantify given the extreme uncertainty at present," he adds.

ICRA’s Nayar has also cut the GDP forecast for FY23 to 7.2 percent from 8 percent.

RBI: Clamp down on inflation or give growth a chance?

Will the RBI MPC play forward defence or will it be on the back foot?

Varma says, “The (RBI) comments we have seen in the last 30 days do seem to suggest that while there is an acknowledgement of upside risks to inflation and downside risk to growth, the overall view seems to be that this is supply side inflation, so there hasn"t really been much of a change (from the previous credit policy review)."

Based on Forbes India’s interactions with economists and analysts, RBI Governor Shaktikanta Das may want to hold fire and pause monetary policy action until June. This could give a clearer indication of the path of inflation, and buy time for growth to catch up meaningfully.

“The RBI may feel compelled to raise rates quickly to stifle inflation. But a rapid rise in interest rates could dampen both investment and spending, and rapidly slow economic growth," observes Cochrane.

In the best-case scenario, the geopolitical conflict ends, inflation cools to 4-5 percent, and growth takes off meaningfully over the next few months. But if the situation takes a turn for the worse, inflation zooms past 6 percent, investments and consumption demand remains bleak, and growth struggles, then consequently the GDP outlook for the next two to three years will be lower.

![]()

“Let’s say we don’t do anything on policy rates and inflation turns out to be much higher than we expect. As a result, after six or nine months the catch-up will be not ‘x’ but ‘4x’ of what we need to do, in which case the growth outlook for the next two to three years will be much lower. So, technically we have given growth a boost in the near 12 months, but basically we are going to bring down medium-term growth," explains Varma.

![]()

Nayar says the monetary policy stance must change to neutral from accommodative no later than June so that inflation expectations do not get anchored. In her opinion, the tone of the policy document will be relatively less dovish, signalling an imminent change of policy stance in June.

“We do think that the RBI should shift the balance of growth and inflation towards anchoring inflation expectations," she adds. She anticipates a cumulative rate hike of 50 basis points in the current calendar year, starting with a reverse repo rate hike in June, followed with two repo rate hikes in August and October.

“Ultimately monetary policy has to do a cost benefit analysis how much are we incrementally supporting growth through our policies versus how much are we risking future growth because of accommodating a higher inflation for so long. It is better to move early than having to do a larger pivot down the line," explains Varma.

“Ultimately monetary policy has to do a cost benefit analysis how much are we incrementally supporting growth through our policies versus how much are we risking future growth because of accommodating a higher inflation for so long. It is better to move early than having to do a larger pivot down the line," explains Varma. Economists have revised their inflation target upwards in light of the volatility in the commodity price cycle in the backdrop of high uncertainty.

Economists have revised their inflation target upwards in light of the volatility in the commodity price cycle in the backdrop of high uncertainty.

Importantly, the investment cycle needs to kick-start to spur durable recovery. Most manufacturing hubs are not operating at full capacity utilisation levels, thereby pent-up demand may not be sufficient to incentivise fresh investments for expansion.

Importantly, the investment cycle needs to kick-start to spur durable recovery. Most manufacturing hubs are not operating at full capacity utilisation levels, thereby pent-up demand may not be sufficient to incentivise fresh investments for expansion. Bhattacharya says there are anecdotal indications of capex plans among MSMEs. He points to strong exports, ancillary signals like bank credit and e-way bills to suggest an uptick in economic activity. “We forecast India’s FY23 GDP growth at 7.8 percent, but there is a strong downside risk to this, which is difficult to quantify given the extreme uncertainty at present," he adds.

Bhattacharya says there are anecdotal indications of capex plans among MSMEs. He points to strong exports, ancillary signals like bank credit and e-way bills to suggest an uptick in economic activity. “We forecast India’s FY23 GDP growth at 7.8 percent, but there is a strong downside risk to this, which is difficult to quantify given the extreme uncertainty at present," he adds.