Ultratech signs on Kesoram Cement's dotted line

With the acquisition of Kesoram's cement business Ultratech stretches its lead with Adani Cement

Last Updated: Dec 01, 2023, 15:15 IST3 min

India’s cement majors are on an expansion-through-acquisition spree. Three months after Adani Cement moved to acquire smaller rival Sanghi Industries, its larger rival Ultratech Cement has moved in to acquire Kesoram Industries’ cement business in an all-stock deal.

The move was widely expected as Kesoram Industries had demerged its tyres and rayon business in 2019 and 2022 respectively. The market had been waiting for the last three years for Kumar Mangalam Birla, the grandson of BK Birla, to take over its cement business. Industry insiders say the cement operations were already being informally run by personnel from Ultratech. Kesoram Industries is owned by Manjushree Khaitan, Kumar Mangalam’s aunt, who took over in 2019 after the death of her father BK Birla.

Ultratech acquired the 10.75 million tons on offer in an all-stock deal with 52 equity shares of Kesoram Industries being swapped for 1 share in Ultratech. The price reflected a 34 percent premium over the closing price of Kesoram Industries on November 30 and valued the cement business at Rs 5,379 crore. Including debt the deal is valued at about Rs 7,600 crore. Ultratech’s share capital will rise by Rs 294 crore.

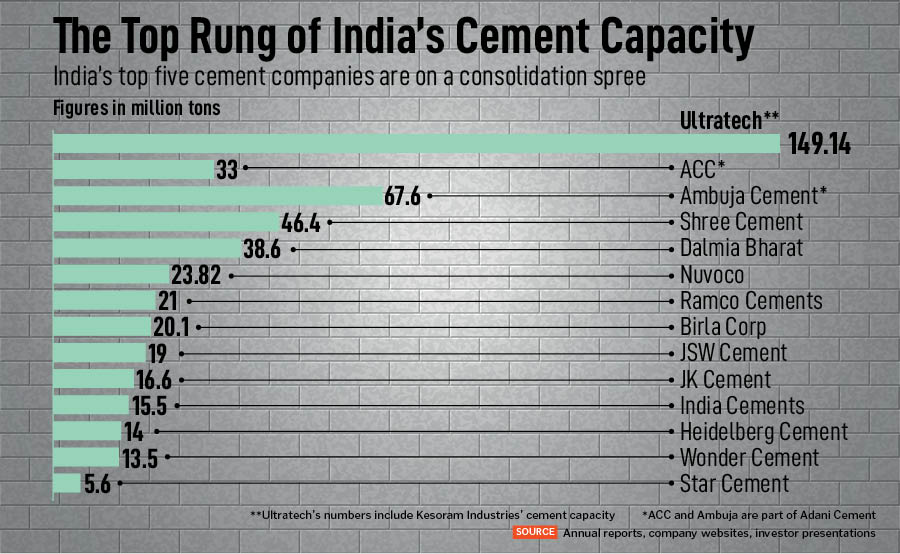

The acquisition comes as Ultratech is moving quickly towards achieving its goal of reaching 200 million tons in cement capacity. At present its capacity stands at 149.14 million tons, making it the world’s largest cement producer outside of China.

The last year has seen quick moves by cement companies to consolidate their positions. A key ingredient has been the fact that now mines are almost always automatically transferred in case of an acquisition. This makes it much easier for companies to justify the price paid. Add to that the fact that a brownfield asset cuts down by at least three years the time taken to expand capacity and it is not hard to see why companies are choosing the acquisition route.

According to Amit Khurana, head of equities at Dolat Capital, $85 is a fair price to pay for the acquisition given the vintage of the assets. In August 2022 when Adani had acquired ACC and Ambuja it paid a hefty premium of $140-160 per ton as that gave it overnight market entry. It costs $100-120 to construct a greenfield plant in India and so there is a discount for old assets.

Part of the reason why companies have been scrambling to ring fence assets and capacity has been the steady growth in construction activity. In Q2 GDP data released on November 30, construction activity rose at 13.3 percent pointing to healthy growth in demand. The Kesoram deal was keenly awaited by the market as it gives Ultratech an entry into Telangana, a state it is not present in.

As large cement companies move to grow faster the market is clearly looking at smaller ones as acquisition targets. One indicator of this is the manner in which the two are priced by the market.

For larger businesses—Ultratech, ACC, Ambuja, Shree, Dalmia—that are in the race to acquire companies, the market is pricing them like growth stocks. Ultratech, for instance, trades at 45 times earnings while ACC, Ambuja, Dalmia Bharat all trade upwards of 25 times. Shree Cement trades at 51 times. Several years of steady growth have been priced in.

Unlike paints and consumer goods cement is a very regional play on account of high transportation costs. As a result, acquiring capacity in a region is often the quickest way to entry as sending goods from far away even to enter a market is not a feasible option. The market has realised that larger companies are willing to pay up for smaller buys in the 5-10 million ton range. The very small 1-2 million ton units have seen no interest as they would result in operations being spread very thin.

Take a look at how the market is pricing smaller companies when compared to their larger rivals. Ramco Cements based in southern India is valued at 60 times earnings. Heidelberg is at 33 times while Sagar Cement is at 218 times. All these businesses may gain if larger rivals continue to consolidate. As the hunt for capacity and limestone gets harder expect competitors to make a move on them.

First Published: Dec 01, 2023, 15:15

Subscribe Now