The quick U-turn from ‘stimulating’ growth to ‘curbing’ inflation has presented policymakers with challenging and risky trade-offs. Uncontrolled and rampant inflation can wipe out decades of growth and upset macroeconomic stability, which can take years to restore. But, beyond a point, to water down growth to cool inflation can rust the economic engine and result in an equally adverse chain of outcomes.

The uniqueness of this conundrum means the pivot point is open to a range of interpretations--of the same data points--in an uncertain and volatile global economy. So, when the world’s largest economy and the biggest source of capital says it is determined to stamp out inflation even at the cost of a recession, it has a forceful impact on markets worldwide.

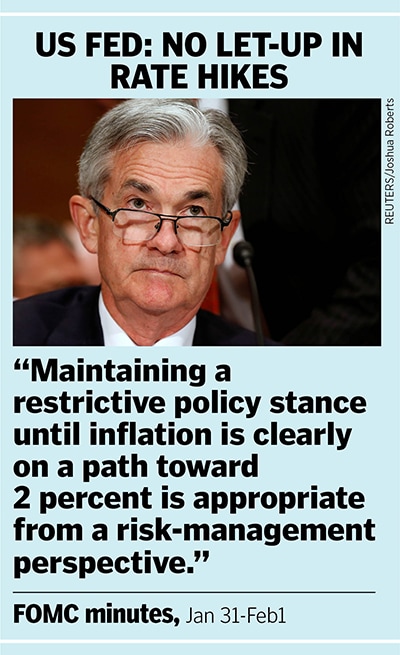

After decades of low interest rates and easy money, the US Fed has hiked interest rates by 450 basis points since March 2022 to bring down inflation to its target of 2 percent. Minutes of the Federal Open Market Committee (FOMC) meeting on January 31-February 1 suggest a wide majority of its members believe that the upside risks to inflation persist.

The current policy rate is between 4.5 percent and 4.75 percent and it is likely to touch 5.6 percent by year-end according to market estimates. Other important policy cues include increasing bond yields, high commodity prices, the rise of the greenback against most other currencies, and the dent in equity valuations. The ripple effect of these on global economies cannot be underestimated.

RBI: Taper the pace of rate hike

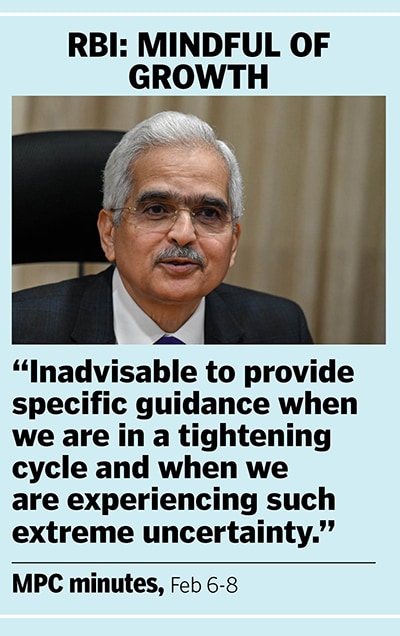

After holding the repo rate at a historic low of 4 percent, the Reserve Bank’s Monetary Policy Committee rushed to hike rates by 40 basis points in an off-cycle meeting in May last year. Since then, it has increased the benchmark rate to its current level of 6.5 percent. The downtrend in the inflation trajectory led many economists and analysts to believe the 25 basis points rate hike announced in the previous policy meeting this month would be the last rate hike this year.

Until May last year, the six-member rate-setting panel stated its willingness to do whatever it takes to support durable recovery even though inflation over-shot its target of 6 percent. Over the past ten months it has shifted its priority to its original mandate of inflation control, and its policy stance has been to focus on withdrawal of accommodation. The RBI has refrained from forward guidance but has reiterated its resolve to remain agile and respond to incoming data. However, the latest MPC minutes suggest there is a divergence in policy priorities among its members.

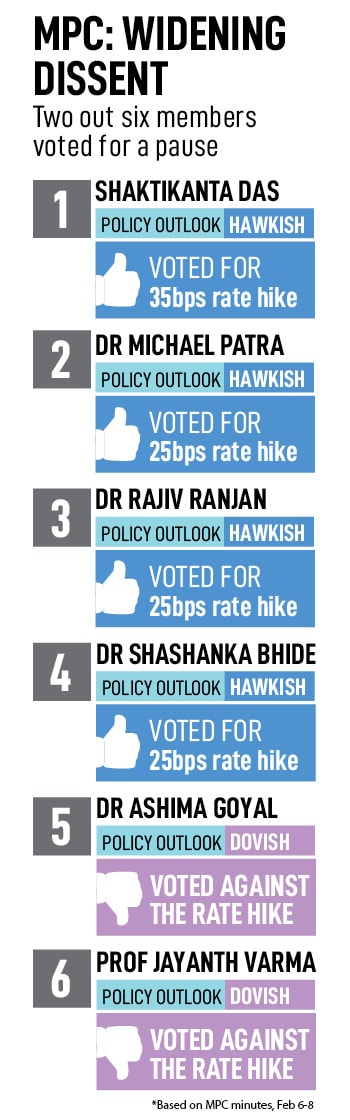

In the December meeting, one of the six members voted for a pause and two members voted against continuation of the policy stance. Recently, in the February meeting, two members voted against the rate hike and policy stance. The growing gap in consensus highlights the complex policy dilemma: To sacrifice growth or fight inflation?

MPC: Split deepens

In the policy meet this month, Ashima Goyal and Jayanth Varma, external members of the MPC, voted against the majority decision of a rate hike of 25 basis points and the continuation of the current policy stance.

![]() “In the second half of 2021-22, monetary policy was complacent about inflation, and we are paying the price for that in terms of unacceptably high inflation in 2022-23. In the second half of 2022-23, monetary policy has, in my view, become complacent about growth, and I fervently hope that we do not pay the price for this in terms of unacceptably low growth in 2023-24," Varma argued.

“In the second half of 2021-22, monetary policy was complacent about inflation, and we are paying the price for that in terms of unacceptably high inflation in 2022-23. In the second half of 2022-23, monetary policy has, in my view, become complacent about growth, and I fervently hope that we do not pay the price for this in terms of unacceptably low growth in 2023-24," Varma argued.

Goyal argued over-tightening does not necessarily improve the future as inflation can rise over time because supply bottlenecks worsen. Furthermore, according to Goyal, the inflation situation in India is very different from that in the US and the actions of the US Fed must not influence domestic monetary policy. Besides, raising real policy rates to reduce demand can have a stronger effect on growth than inflation, Goyal observed.

“Since there are more lags in monetary transmission in India, over-shooting can have persistent deleterious effects here, including instability. Macroeconomic stability improves most rapidly if real interest rates are kept smoothly below growth rates and counter external shocks," Goyal added.

Of the six members, RBI Governor Shaktikanta Das was the most cautious. Das proposed a 35 basis points rate hike to tackle core inflation which rose to 6.52 percent in January in comparison to a 12-month low of 5.72 percent in December.

![]() “The minutes of the MPC meeting showed diverging policy priorities for the hawks and doves-–the former expressing concerns about the stickiness of inflation, while the latter warned of the risk of a policy overshoot. After 325bp of cumulative rate hikes having already been delivered in a span of 10 months, assessing the policy impact is critical and merely reacting to past inflation readings will be backward-looking monetary policy. We believe this is what is driving the divergence between the two external MPC members, who are forward-looking, versus the hawks, who are more focused on concurrent data," say brokerage firm Nomura’s economists.

“The minutes of the MPC meeting showed diverging policy priorities for the hawks and doves-–the former expressing concerns about the stickiness of inflation, while the latter warned of the risk of a policy overshoot. After 325bp of cumulative rate hikes having already been delivered in a span of 10 months, assessing the policy impact is critical and merely reacting to past inflation readings will be backward-looking monetary policy. We believe this is what is driving the divergence between the two external MPC members, who are forward-looking, versus the hawks, who are more focused on concurrent data," say brokerage firm Nomura’s economists.

What Goyal and Varma see as overtightening the other four members see as a code to crack persistent high core inflation.

Governor Das said, “Disinflation towards the target rate is likely to be protracted given the stickiness of core inflation at elevated levels. Durability of a disinflation process cannot solely rely on food inflation. There is considerable uncertainty at this stage on the evolving inflation trajectory due to ongoing geopolitical tensions, global financial market volatility, rising non-oil commodity prices, volatile crude oil prices, and also weather-related events."

Rajiv Ranjan, ED, RBI, agreed, “The persistence of inflation, however, can lead to large repricing of risk with consequent market turmoil. It will be premature to lower the guard on inflation as the credibility of central banks in fighting inflation has large ramifications for stabilisation of inflation and firm anchoring of inflation expectations."

Shashanka Bhide, external member at RBI, said, “Persistence of core inflation at a high level is a crucial concern at this stage. It is important to reduce the demand side pressures on inflation and bring the inflation expectations of the various stakeholders closer to the policy target to sustain the growth momentum."

RBI deputy governor Michael Patra held a very cautious outlook for inflation and said the stance of monetary policy will need to remain disinflationary till inflation returns to target.

“Although it seems to have peaked, inflation remains high and, in my view, it is the biggest threat to the macroeconomic outlook. Restoration of price stability-–as statutorily mandated-–will provide a solid foundation for a growth trajectory that actualises India’s potential. Taking into account the height of inflation, current and projected, monetary and financial conditions still reflect some slack, although they are moving into tighter territory with the follow through of recent monetary policy actions. The issue is one of timing," Patra said.

Nomura expects GDP growth to decline to 5.3 percent in FY24 and sees retail inflation average at 4.8 percent versus the RBI estimate of 5.3 percent. On this basis, the brokerage firm believes there could be a pause in the policy rate hike cycle and doesn’t rule out the start of a rate easing cycle from October. Most analysts and economists have pencilled a rate hike of 25 basis points in the upcoming monetary policy meeting in April.

“Participants observed that a restrictive policy stance would need to be maintained until the incoming data provided confidence that inflation was on a sustained downward path to 2 percent, which was likely to take some time," said the minutes of the previous FOMC meeting.

“Participants observed that a restrictive policy stance would need to be maintained until the incoming data provided confidence that inflation was on a sustained downward path to 2 percent, which was likely to take some time," said the minutes of the previous FOMC meeting. “In the second half of 2021-22, monetary policy was complacent about inflation, and we are paying the price for that in terms of unacceptably high inflation in 2022-23. In the second half of 2022-23, monetary policy has, in my view, become complacent about growth, and I fervently hope that we do not pay the price for this in terms of unacceptably low growth in 2023-24," Varma argued.

“In the second half of 2021-22, monetary policy was complacent about inflation, and we are paying the price for that in terms of unacceptably high inflation in 2022-23. In the second half of 2022-23, monetary policy has, in my view, become complacent about growth, and I fervently hope that we do not pay the price for this in terms of unacceptably low growth in 2023-24," Varma argued. “The minutes of the MPC meeting showed diverging policy priorities for the hawks and doves-–the former expressing concerns about the stickiness of inflation, while the latter warned of the risk of a policy overshoot. After 325bp of cumulative rate hikes having already been delivered in a span of 10 months, assessing the policy impact is critical and merely reacting to past inflation readings will be backward-looking monetary policy. We believe this is what is driving the divergence between the two external MPC members, who are forward-looking, versus the hawks, who are more focused on concurrent data," say brokerage firm Nomura’s economists.

“The minutes of the MPC meeting showed diverging policy priorities for the hawks and doves-–the former expressing concerns about the stickiness of inflation, while the latter warned of the risk of a policy overshoot. After 325bp of cumulative rate hikes having already been delivered in a span of 10 months, assessing the policy impact is critical and merely reacting to past inflation readings will be backward-looking monetary policy. We believe this is what is driving the divergence between the two external MPC members, who are forward-looking, versus the hawks, who are more focused on concurrent data," say brokerage firm Nomura’s economists.